To see my first post on Wells Fargo, click here: Wells Fargo (WFC)

At under $44 a share on August 15th, I’m finding the stock to be very attractively priced at this point. Wells Fargo continues to get punished by the market, largely due to declining interest rates, an inverted yield curve, and recession fears. These are legitimate risks worth assessing, however I find the fears to be overblown as a lot of these risks were already priced into the stock. A reversal in any of these trends or a shift in sentiment may cause the stock to rapidly correct upward due to strong capital returns.

Rates

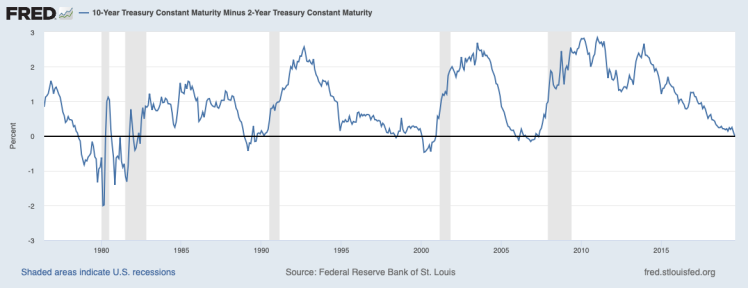

At their latest meeting in July, the Federal Reserve cut interest rates 25 basis points to sustain the expansion of the economy. This is somewhat bad news for banks, as it reduces the interest they can earn on assets. While they can lower the rates paid on deposits, it isn’t a one for one offset and it’s unlikely to completely make up for the lost income. Also, this week, the 2-year treasury yield surpassed the 10-year yield, which further pressures net interest margins as banks borrow short and lend long.

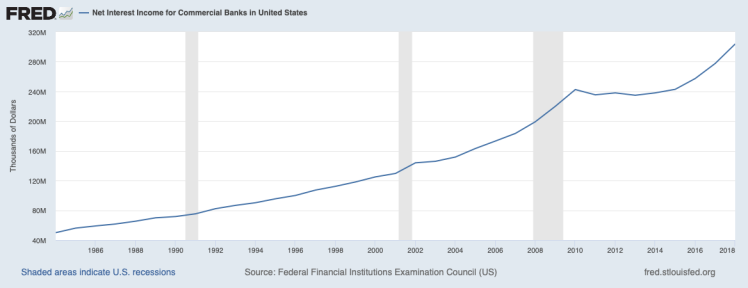

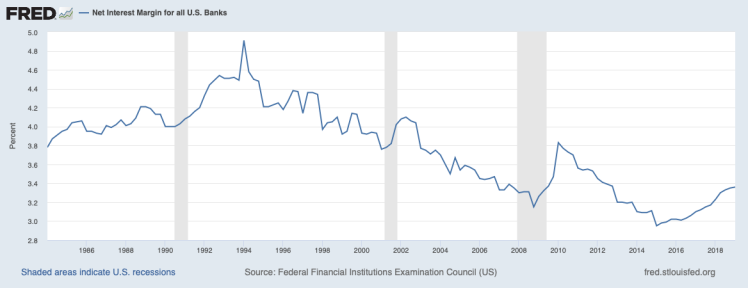

John Huber, portfolio manager at Saber Capital Management, recently made a note on Twitter regarding the history of U.S. bank net interest income that promotes a longer term view than the one the market seems to be adopting currently. Since rates peaked in 1982, net interest income in the banking system has risen in all but two years while rates declined and, generally, net interest margins compressed.

Put simply, banking profits continue to rise over the long run regardless of what’s going on with rates at any given point in time. The key factor for the long term investor’s profits is growth in the economy and banking assets, as rates are bound to be at a different level and headed in a different direction at any point in the future.

In Wells Fargo’s quarterly report, they also outlined the effect of interest rates declines. As of 6/30/19, if there were a 100 basis point decrease in rates, it is estimated that net interest income would be down $0.7 – $1.2 billion in the first year and $2.6 – $3.1 billion in year two. This effect would result in declines of roughly 5% and 14%, respectively, in net income if there were no offsetting pickup in business, which I find unlikely. In a case of lower rates, there would likely be a pick-up in economic activity and borrowing, which would generate substantial fees for the non-interest income side of Wells Fargo as they originate massive amounts of loans. This is the benefit of the resiliency of Wells Fargo’s diversified banking business. While this situation would certainly present headwinds, it appears to have limited downside, be short-term in nature, and it hasn’t even come to fruition yet.

Credit Quality

The inverted yield curve has the market betting more and more on a recession occurring in the near future, which may come true but is nearly impossible to predict. One thing that is certain is that we will experience a downturn eventually. Thanks to the Fed’s asset cap placed on Wells Fargo, they are as prepared as any of the banks to weather an economic storm due to the high credit quality of their loans.

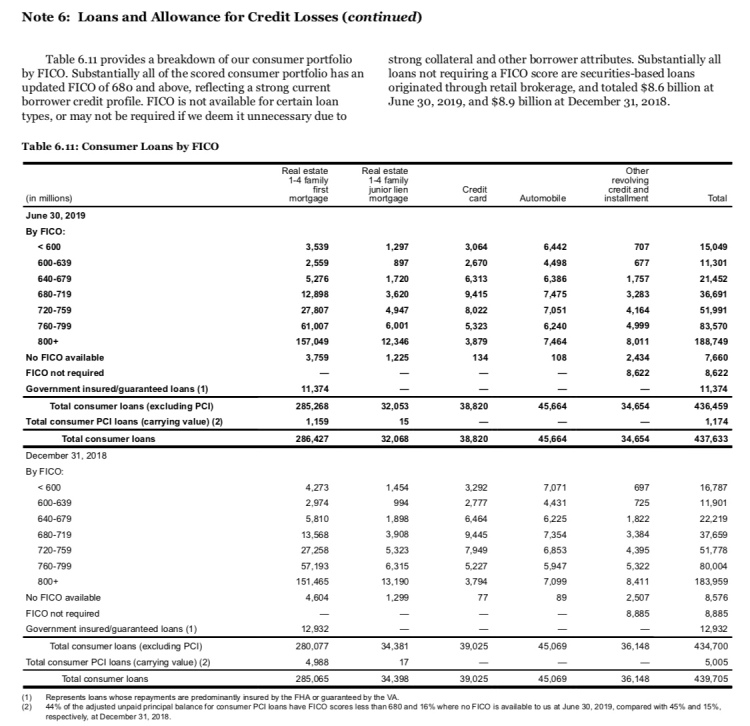

In their recent quarterly report, the consumer loan segment showed markable improvement in credit quality. Just because the bank can’t grow assets doesn’t mean it can’t grow quality and in turn strengthen its earnings resiliency. Here’s a look at the FICO score mix changes from 12/31/18 to 6/30/19:

In the first half of 2019, total consumer loans were up just $1.76 billion, or 0.4%, but this minuscule change due to the asset cap doesn’t paint the full picture. Loans to FICOs above 720 increased $8.57 billion, or 2.7%, and $4.79 billion of that increase came in the highest quality 800+ FICO segment, which was up 2.6% in the first six months of the year. That’s not all. Loans in which the highest loss rates will arise in a recession continued to decline. Loans to FICOs under 720 decreased $4.07 billion, or 4.6%. The low quality PCI loans purchased from Wachovia were also down almost $4 billion.

And this is just through six months. Wells Fargo is pruning its balance sheet. Because they aren’t allowed to grow, the next best thing is to minimize the loans that will generate the most loss and grow the highest quality loans. Therefore, Wells Fargo is continuing to grow in quality.

Buybacks

On the company’s third quarter conference call, the CFO reiterated the capital plan which will return $32.1 billion to shareholders in the next year. $23 billion of that will come through share buybacks and he stated that they plan to front load the program with 65% of the buybacks occurring in the first two quarters. That would be $15 billion in six months and over $117 million per trading day through December, which can retire over 2.7 million shares a day at the closing price of $43.38 on 8/15/19.

The six month buyback figure of $15 billion is equal to 7.8% of the current market cap. If the share price remains in this area through the end of 2019, the company could very well retire over 7% of the shares outstanding by New Years. Notably, this is being done at five-year low valuation multiples for a company making a pretty steady $20 billion or so (give or take 5-10%) a year.

I think the probability that the summer and fall of 2019 buybacks make existing long term owners of Wells Fargo a lot of money is fairly high. There just could not be better timing for short term pessimism when you are reinvesting profits into a beaten down stock price.

Happy investing.

Bryce Dooley

Disclosure: I am long WFC.